Mastering the 50-30-20 Rule: A Simple Budgeting Strategy for Financial Success

Budgeting is one of the main abilities of sound financial management. Correct income distribution is essential for both immediate stability and long-term success, regardless of your level of financial responsibility or beginning point. For many people, budgeting at first seems difficult, but applying a consistent, fundamental method will make all the difference. One such approach divides your money into three fundamental categories and is the 50-30-20 Rule, a basic but lethal approach. This Rule helps you manage present needs and wants as well as assures you of saving for your future goals. This post will help you mastering 50-30-20 Rule and provide reasonable recommendations for implementing it into your financial planning.

What is 50-30-20 Rule?

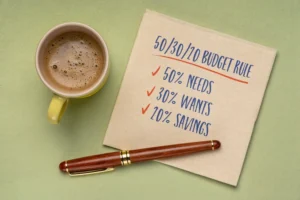

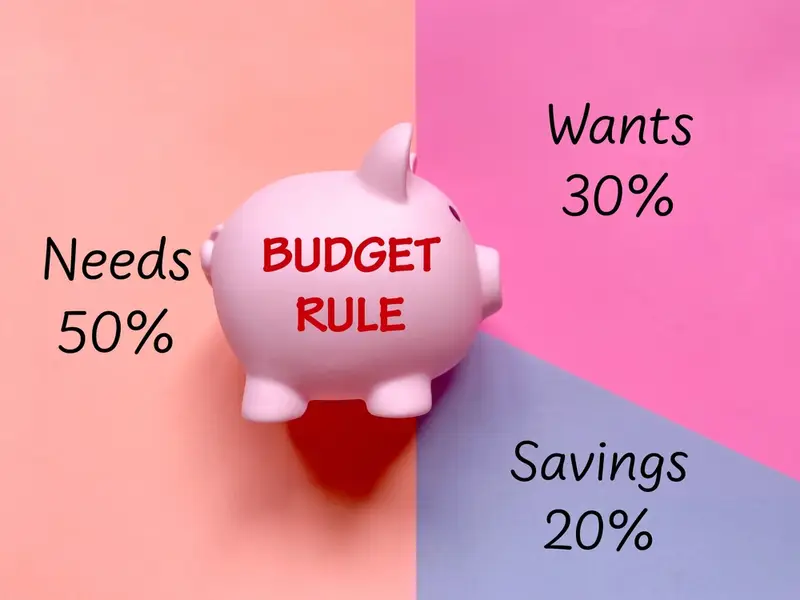

The 50-30-20 Rule is a super personal finance strategy made to simplify budgeting by dividing your finances into three categories:

- 50% Needs: Essential expenses like housing, utilities, groceries, and transportation are compulsory for a basic livelihood.

- 30% Wants: Non-essential spending like entertainment, dining out, hobbies, and travel are added in this section

- 20% Savings: Saving for the future—whether it’s for an emergency fund, retirement, or paying off debt are included in this category

This Rule offers a balanced, dynamic approach to money management, allowing you to enjoy your life while ensuring you are building financial security for the future.

Why the 50-30-20 Rule Works?

One of the 50–30–20 Rule’s best advantages is its noncomplex character. Regardless of their financial condition, anyone can apply its simple and understandable approach. The Rule guarantees that your fundamental needs are satisfied and gives opportunity for personal enjoyment and future planning in addition.

Here are some reasons why this Rule is effective:

- Simplicity: The Rule removes the complexities sometimes linked with budgeting. It’s about looking ahead rather than tracking every single dollar.

- Balanced Approach: The 50-30-20 Rule encourages overall financial stability by helping you maintain a fair balance between your needs, optional expenditures, and savings goals.

- Financial Security: The Rule guarantees that you are ready for unanticipated costs and have a strong basis for long-term financial objectives such as investing or retirement by giving savings a top priority.

Breaking Down Each Category of the 50-30-20 Rule

Breaking out each category and investigating effective management techniques can help you apply the 50-30-20 Rule in your own life.

1. 50% – Needs

“Needs” are the essential living expenses that are for your basic livelihood. These expenses are necessary for your day-to-day life and include:

- Housing: Rental payments, property taxes, and home insurance.

- Utilities: Electricity, water, heating, and internet bills.

- Groceries: The essential food items that you need for daily meals.

- Transportation: Car payments, insurance, fuel, or public transportation fees.

These are the foundations of your financial situation; hence, they should come first over your needs. Still, in this category, you can cut costs without compromising your quality of life. You might look at decreasing your living space, cutting utility use, or finding less costly ways of movement.

2. 30% – Wants

“Wants” are not essential for basic livelihood but involve your happiness and lifestyle. Examples include:

- Entertainment: Streaming subscriptions, concerts, films.

- Dining out: at Restaurants, take-out, or coffee shops.

- Travel: Weekends, vacations, or luxuries, including clothes and electronics.

While it’s important to keep these expenses under control, taking part in some of your wants can improve your overall well-being and provide a sense of balance in life. The way forward is to be aware of your spending and discover less costly methods to enjoy life, including cooking at home more often or choosing less costly holiday plans.

3. 20% – Savings

The magic occurs in the 20% Savings area. Long-term financial success depends on saving for the future—for an emergency fund, for retirement, for other financial objectives.

This category can be divided into three main categories:

- Emergency Fund: Save money for unanticipated costs include medical bills, auto repairs, or job loss in an emergency fund.

- Retirement Savings: Contributing to long-term savings plans.

- Debt Repayment: If you have a lot of debts, dedicating a portion of this 20% towards paying them off can help your financial freedom.

To make this process easier, consider automating your savings through direct deposits or setting up automatic transfers to dedicated savings accounts.

How to Implement the 50-30-20 Rule in Your Life?

Here’s how to start using the 50-30-20 Rule in your daily life:

- Track Your Income and Expenses: Begin by checking all your income sources and understanding where your money is being spent. Keep on top of your money with a spreadsheet or app.

- Categorize Your Spending: Once you have a clear picture of your spending habits, categorize each expense into one of the three categories: Needs, Wants, or Savings.

- Make Adjustments: Based on the allocation, you may need to make adjustments. If you find that you’re spending too much on wants or not saving enough, shuffle your budget until it feels right.

- Monitor and Review: Your financial situation may change over time, so regularly review and adjust your budget to stay aligned with the 50-30-20 Rule.

Common Pitfalls to Avoid When Following the 50-30-20 Rule

While the mastering the 50-30-20 Rule is simple, there are some common budgeting mistakes that people make when sticking to it:

- Overspending on Wants: It’s easy to get carried away with optional spending, especially when there’s room in the budget. Be mindful of keeping this category in check to avoid negatively impacting your savings.

- High Fixed Costs: If you live in an area with high housing or transportation costs, it may be difficult to stick to the 50% needs category. In these cases, consider adjusting your spending in other ways.

- Lack of Flexibility: While it’s important to maintain balance, it’s also crucial to be flexible. If you have a month where you need to spend more on needs (e.g., medical expenses), it’s okay to adjust other categories for a while.

Adapting the 50-30-20 Rule for Different Lifestyles

The 50-30-20 Rule is adaptable to various financial situations, including:

- Irregular Income: For freelancers or gig workers, the Rule can be adjusted by averaging income over several months. This ensures that you always have a balanced approach, even during fluctuating months.

- High-Cost Areas: If you live in a high-cost city, you may need to allocate a larger portion of your income to needs. In such cases, it’s essential to be mindful of optional spending and focus more on savings.

- Aggressive Savings: For those aiming for early retirement or paying off significant debt, you may choose to adjust the Rule by allocating more to savings and reducing optional spending.

Alternatives to the Mastering the 50-30-20 Rule

While the 50-30-20 Rule is widely recommended, other budgeting methods might work better for some folks:

- Zero-Based Budgeting: Every dollar is given a specific job, whether it’s for needs, wants, or savings.

- Envelope System: Cash is physically divided into envelopes for each spending category, helping to control spending.

- 80-20 Rule: This variation focuses on saving 20% of your income, with the remaining 80% covering your needs and wants.

Tools and Resources to Help You Stick to the 50-30-20 Rule

There are plenty of tools to help you manage your budget:

- Budgeting Apps: Tools like Mint, YNAB (You Need a Budget), and Personal Capital can help you track income and expenses.

- Spreadsheets: Google Sheets and Excel offer customizable templates to manage your finances.

- Financial Advisors: For personalized advice, a financial planner can help you stick to the 50-30-20 Rule and plan for future goals.

Conclusion: Mastering the 50-30-20 Rule

Anyone may help themselves take control of their money by using the simple and useful 50-30-20 Rule for personal budgeting. This guideline offers a basic yet efficient structure for budgeting whether your financial habits need improvement or you are just beginning. Concentrating on your requirements, wants, and savings will help you strike a good balance, promoting financial stability.

Start following this guideline right now to be on your road to financial mastery. Comment below with your experiences or ask any queries; we would be very happy to hear from you!

FAQs about the 50-30-20 Rule

- Can I adjust the percentages based on my needs? If your financial circumstances call for it, sure, you can change the percentages. If your fixed expenses are considerable, for instance, you could assign more to needs and momentarily lower the share for wants or savings.

- How do I handle debt while following the 50-30-20 Rule? Under the savings category, you can include debt payback; alternatively, you can change your wants % to direct more toward debt pay-off. First, give high-interest debt top priority.

- What if I have a low income? How can I save 20%? Try for a smaller percentage if limited income makes saving 20% impractical. As your income rises, concentrate on reducing non-essential expenses (wants) and steadily build your savings.

- Is mastering the 50-30-20 rule suitable for families? Indeed, families will find it flexible. If your family’s spending is more, you could have to change the necessities category; still, most household budgets find the general structure to be rather effective.

- Can the 50-30-20 Rule help me with paying off student loans? Indeed, you can pay your student loans from a part of the savings category. Should loan pay-off top importance, you might spend more of your savings on debt service and modify other areas.